The mandatory application of IFRS 16 is approaching and the majority of our customers are already working on adapting their internal processes to the challenges of the new standard. Thanks to the experience gained from initial projects and the "Group Accounting Working Group" initiated by us, we are in a position to actively assist you with the operational challenges arising from the amendments to IFRS 16.

What is IFRS 16?

International Financial Reporting Standard 16 - Leases (IFRS 16) is an accounting standard issued by the IASB. IFRS 16 replaces IAS 17.

What are the current challenges posed by the publication of the new standard?

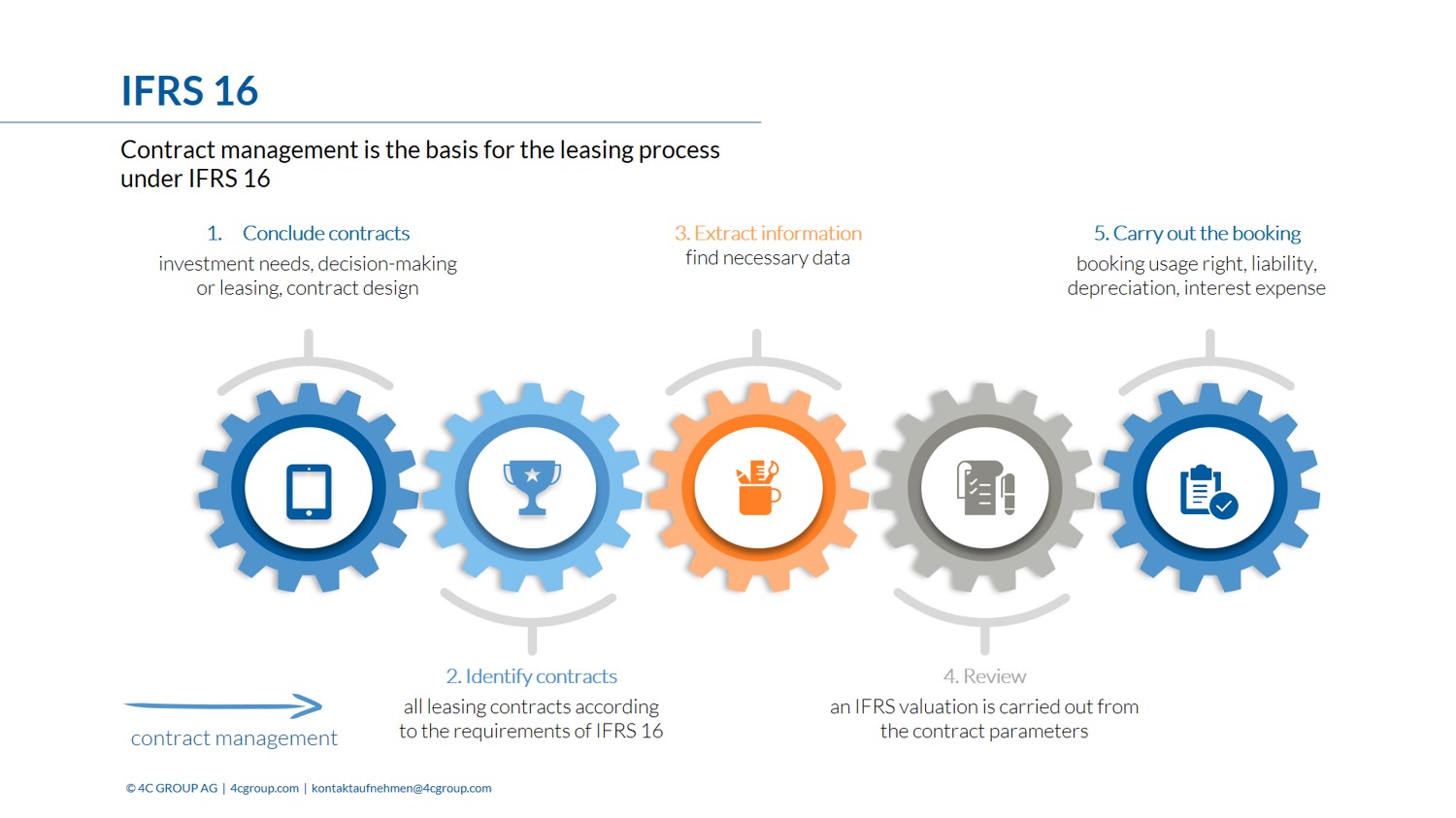

IFRS 16 poses practical challenges for companies with regard to complete contract management. These relate both to the organisational and procedural handling of leases, including IT support on the system side. The challenge lies not only in the one-off conversion from IAS 17 to IFRS 16, but also in the continuous recording of all leasing contracts in the future. The automatic provision of the information required for accounting will necessitate a reorganisation of the process organisation and the provision of suitable system support. The prerequisite for this is the implementation of resilient processes.

In addition to the effects on the balance sheet, the biggest challenge is the procedural handling of leasing relationships with the associated system support concept. For this reason, responsibilities must be defined within the group and in the individual companies and linked to resilient processes. Due to the increased need for information, the future system architecture, which must be implemented for each process step, represents a critical success factor. As a consequence of the changed regulations, higher personnel and time capacities are often required to map leasing relationships.

Standardised procedure model for implementing the requirements of IFRS 16

4C GROUP's approach focuses on operational challenges to fundamentally realign processes. For this reason, a standardised procedure model was developed to implement the requirements of IFRS 16.

Standardised process model:

- Inventory on the basis of a standardised analysis model for the actual assessment of rental and leasing relationships: Analysis of the existing processes and the transparency of contract management. An evaluation matrix for the effects shows the relevance for the fields of action in the company.

- The initial changeover is planned on the basis of the analysis.

- Organizational implementation through the definition of responsibilities

- Adjustment of the workflow processes

- Definition and adaptation of the required system support

IFRS 16 at a Glance

Get all the information you need at a glance in our whitepaper on IFRS 16.