Start Your Expedition

Disclosure Management: The Revolution in Reporting

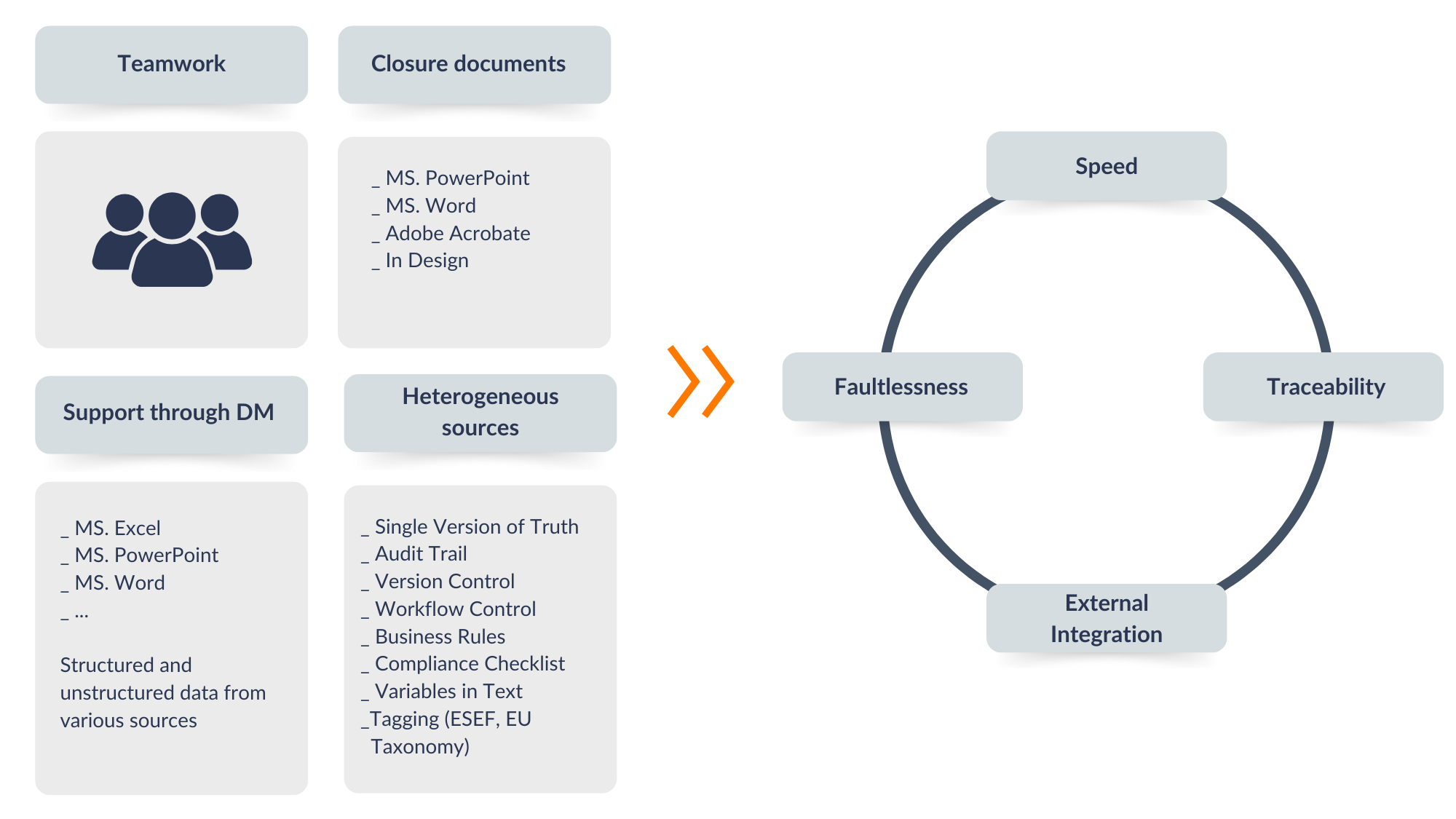

The increasing demands on companies to provide reporting in a variety of forms represent a growing challenge. From annual financial statements and annual reports to sustainability reports and digital information - the range is enormous. As a result, numerous employees in the company are involved in creating these reports, which raises questions about access rights, change tracking and data consistency. This need for customized information for different recipients is omnipresent.

Without a clear target image of the future finance organization, the CFO department will become the dinosaur of the company!

Your Benefits

Disclosure management solves the problem of complex and time-consuming reporting. This applies in particular to companies that have to fulfill reporting obligations for various recipients. C-level executives, financial managers and reporting staff will benefit significantly from Disclosure Management. For companies, this means a considerable increase in efficiency in reporting, which ensures consistency and traceability. At the same time, they will be able to meet the growing demands for different reports without wasting time and resources.

- Real-time insights: Time savings: Automation reduces manual workload.

- Consistency and quality improvement: Consistent data minimizes errors and results in greater accuracy in reports.

- Traceability: Changes can be accurately tracked and authorized.

- Adaptability and integration: Respond to changing requirements and taxonomies and seamlessly integrate different data sources.

- Digital tagging: Facilitates compliance with sustainability reporting rules.

- Risk reduction: Prevents errors and misinformation.

-

Competitive advantage: Faster and more efficient reporting.

Our Services at a Glance

|

Success Factors

Success Factors for the Implementation of Disclosure Management

The successful implementation of disclosure management requires careful planning and implementation.

Clear Process Definition

It is crucial to clearly define and document the reporting processes within the company.

Integration of Data Sources

The seamless integration of different data sources is of central importance to ensure up-to-date information.

Training and Support

Employees must be trained and supported in the use of disclosure management tools.

Adaptability

The flexibility of the tools enables adaptation to changing requirements and taxonomies.

Client Testimonials

"With the IBM platform we have created a solution with which we have integrated and automated consolidation, forecasting, planning and reporting. The 4C GROUP supported us fully from the conception to the implementation and rollout. At the same time, an internal team was set up and trained so that we are able to carry out further developments ourselves as far as possible and use Planning Analytics as our "performance hub"."

Why 4C?

Why we are the Ideal Partner

- Experience: As an experienced management consultancy, we have successfully supported numerous companies with disclosure management.

- Expert knowledge: Our experts have in-depth knowledge of reporting and disclosure management.

- Customer-centric approach: Our solutions are tailor-made and offer continuous support to meet your individual requirements..

Contact us today to optimize your reporting processes and reap the benefits of disclosure management. We are your partner for efficient, transparent and consistent reporting.

Do you have any questions or would you like to find out more about our services?

Contact us for a non-binding consultation.

Your Experts

More Topics

Contact Us

We would like to point out that this website provides only a limited insight into our services. Our expertise and range of services cannot be fully represented on this platform. For personalized consultation and to address your specific concerns in the best possible way, we warmly invite you to contact us directly to offer you tailor-made solutions.

Thank you for your trust. We look forward to hearing from you.

{kind=link}