Start Your Expedition

Sales Management - Efficient Management for Your Sales Organization

Successful sales management requires the cooperation of two different personality types: The thoroughbred salesperson who focuses on interpersonal relationships and closing deals and the numbers person who strives for structural insights from data. The central question is: How can these different perspectives lead to success?

Sales Management: Challenge or Opportunity?

Sales management aims to optimize sales results, increase market shares and sales volumes, improve margins and optimize delivery capacity and working capital through precise forecasting. However, the customer's interests and satisfaction must never be lost sight of.

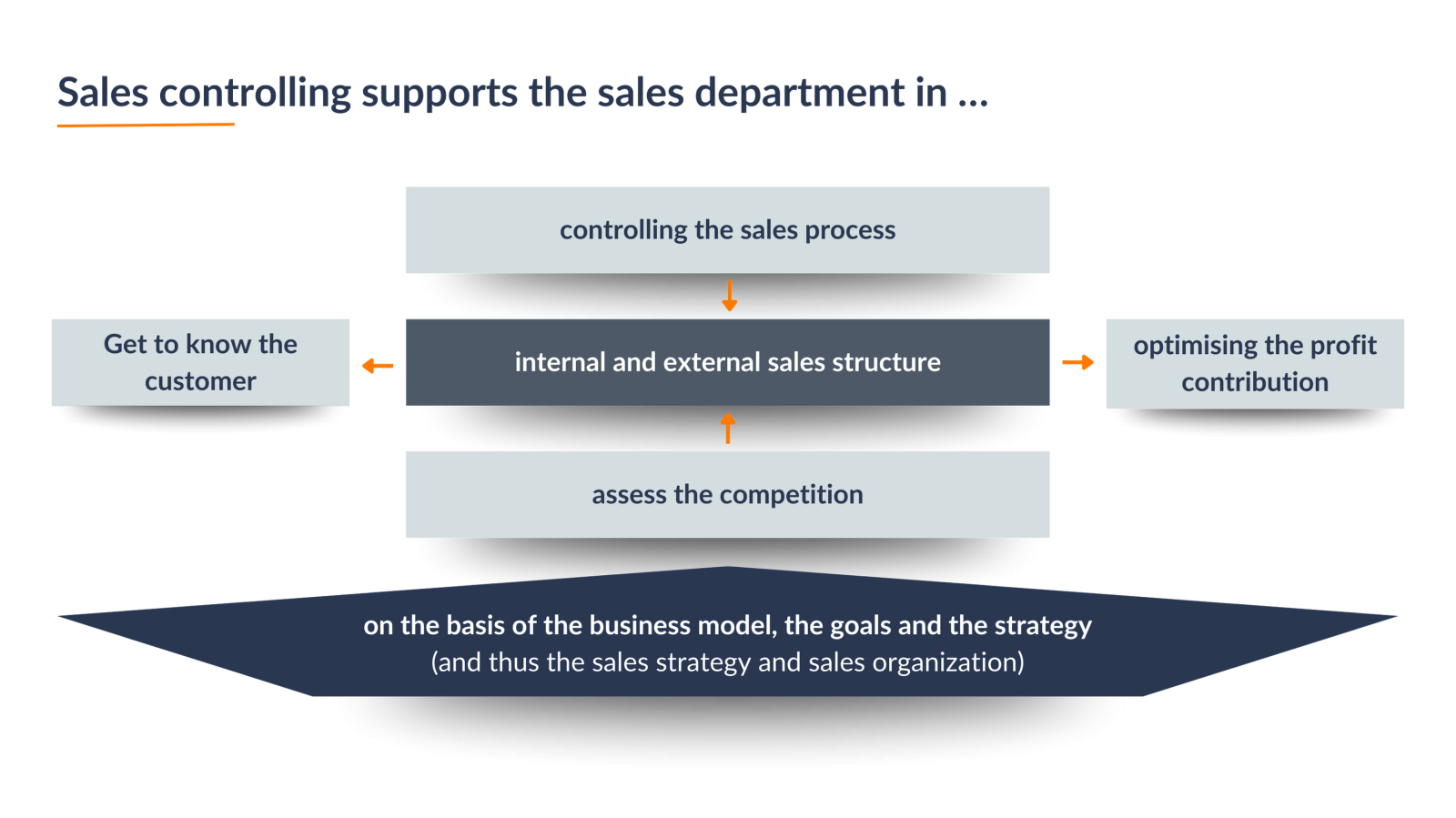

Sales management must be derived from the business model and strategy, as B2B and B2C business models, stationary and online sales as well as own and partner sales function differently. These differences not only influence sales management, but also the sales process.

Prioritization and Success Monitoring: Setting priorities and monitoring success are key. To do this, the sales employee must know the customer, channel or partner and their contribution to success. This includes both long-term (segmentation, targeting) and short-term activities (visit planning, event preparation).

Synergy Between Sales and Management: Despite initial skepticism about transparency, more effective sales processes, focused customer approaches and improved lead generation lead to a win-win situation for both sides.

Sales Management as a Competitive Advantage: Tools and information: implementing tools that support sales and provide relevant information offers a competitive advantage. This includes customer-specific reporting, planning and forecasting systems that are tailored to sales needs, as well as the use of modern methods such as predictive analytics.

Simplicity and Clarity: The tools should be easy to use and present the quotation processes and their impact on the company in a transparent manner. An appealing design also increases acceptance in sales.

4C GROUP transforms the challenge of sales management into an opportunity for growth. With a focus on customized solutions that consider both analytical depth and interpersonal dynamics, we help you achieve your sales objectives efficiently and effectively.

Success Factors

-

Strategic Alignment and Customer Focus: Developing a sales strategy that is closely aligned with market conditions and customer needs, including a deep understanding of target customers and tailoring the offering to meet these needs.

-

Goal Setting and Performance Management: Definition of clear, specific and measurable sales goals that align with business objectives, complemented by consistent performance measurement through KPIs and regular feedback to drive continuous performance improvement.

-

Technology and Data Analysis: Intensive use of CRM systems and data analysis to optimize customer management and use of modern technologies to increase efficiency in the sales process.

-

Training and Development of the Sales Team: Engagement in regular training and development programs to continuously improve the skills of the sales team and ensure high sales effectiveness.

-

Flexibility, Communication and Customer Relations: Promote flexibility in strategies to quickly adapt to market changes, strengthen internal communication and teamwork, and build and maintain long-term customer relationships to ensure sustainable business development.

These factors make a decisive contribution to the effectiveness of sales management and the long-term success of the company. Does your company already meet these requirements? Contact our experts directly to maximize the success of your sales management.

Do you have any questions or would you like to find out more about our services?

Contact us for a non-binding consultation.

Your Benefits

Efficiency and Effectiveness

Sales management makes it possible to organize sales activities more efficiently and effectively. Targeted control allows resources such as time and budget to be used optimally, which increases productivity.

Targeted Strategy

Sales management enables the efficient and effective organization of sales activities. Through targeted control, resources such as time and budget can be optimally utilized, which increases productivity.

Improve Customer Understanding

Sales management can lead to a deeper understanding of customer needs and market conditions. This allows for personalized customer engagement and strengthens customer relationships.

Increasing Sales and Measuring Success

Effective sales management can contribute to revenue growth by helping to better identify and leverage sales opportunities. It also allows for the continuous monitoring and analysis of sales performance, which is important for identifying areas for improvement and measuring the success of sales initiatives.

Overall, sales management is a key element for the sustainable success of a company, as it helps to achieve sales objectives strategically, efficiently, and effectively.

Our Approach

Our 4C approach to sales management includes setting clear, measurable objectives that are aligned with customer needs and market conditions. The use of CRM systems and data analysis tools supports efficient customer management and informed decision-making. Regular training and performance evaluations promote a skilled sales team and allow for continuous adjustments to the market. Additionally, strong internal communication and collaboration between sales, marketing, and other departments are crucial for success.

Client Testimonials

"The 4C GROUP pursues a consulting approach that is rarely found today. The combination of professional know-how, procedural expertise and technical competence offers considerable added value, especially in performance management. Concept and implementation go hand in hand and you get not only a presentation of options, but real consulting based on individual requirements".

More Topics

Your Experts

Feel free to contact us

We would like to point out that this website only offers a limited insight into our services. Our expertise and range of services cannot be fully represented on this platform. For individual advice and to address your specific concerns in the best possible way, we cordially invite you to contact us directly so that we can offer you tailor-made solutions.

Thank you for your trust. We look forward to hearing from you.